In my real estate career, I’ve been blessed to be able to meet people from all walks of life.

In addition to serving fellow Singaporeans like myself, I also serve PRs and foreigners who are looking for a place to stay. This is especially so when I handle rental transactions.

In an open economy like Singapore, people from various nationalities have made Singapore their permanent residence as they live, work and play here.

Most PRs tend to go for rental units – it is far more flexible and allows one to easily make the move back to their home countries if personal circumstances change.

However, I have met some PRs who see Singapore as a permanent home and would like to sink deeper roots into our country.

If you are PR reading this article, let’s explore the feasibility factors of you buying a property here instead of continuously renting.

Factor #1: Rising Rental Costs That Is Similar To A Monthly Mortgage

If you understand Singaporeans well, you will find out that we loathe paying rental. The idea of helping landlords pay off their monthly mortgage doesn’t sit well as we know those are monies paid that we can’t get back.

But by having a mortgage and property ownership, it means we have a chance to recover those monies back if we ever make the decision to sell off the property.

However, we need to find the tipping point where it makes sense to buy rather than continue to rent.

Here’s an example:

In January 2023, you can purchase a 1-bedder resale unit at $850K at Whistler Grand.

Assuming you take a 75% LTV loan with an interest rate of 4.3%, this means the monthly mortgage is about $3.2K per month.

Compare this to paying a monthly rental of almost $3900 per month at the same location.

When you pay your monthly rental, all the monies is considered gone and is impossible to recover.

But when you choose to pay a monthly mortgage, a portion of it goes to your equity and ownership of the property.

And you can recover back these monies when you choose to sell off the property in the future.

At the same time, as you pay down your mortgage every month – the principal will go down.

This means the interest paid will slowly be reduced and you accumulate more equity.

At such high rental rates, perhaps buying a unit instead can be the better financial decision.

Factor #2: Currency Risks

As a PR, you may have assets and income in different currencies, which can expose you to currency risks.

If you are a Malaysian with Singapore PR, you would have noticed the currency risks of buying Malaysian property.

Over the past few years, parking your monies in Malaysian Ringgit would have resulted in losses as SGD grew in strength.

Over the past 10 years, the MYR has lost 25% of its value when compared to SGD.

This is significant.

That being said, the Singapore currency does fluctuate from time to time.

Factor #3: The 5% ABSD Rate for Singapore PRs

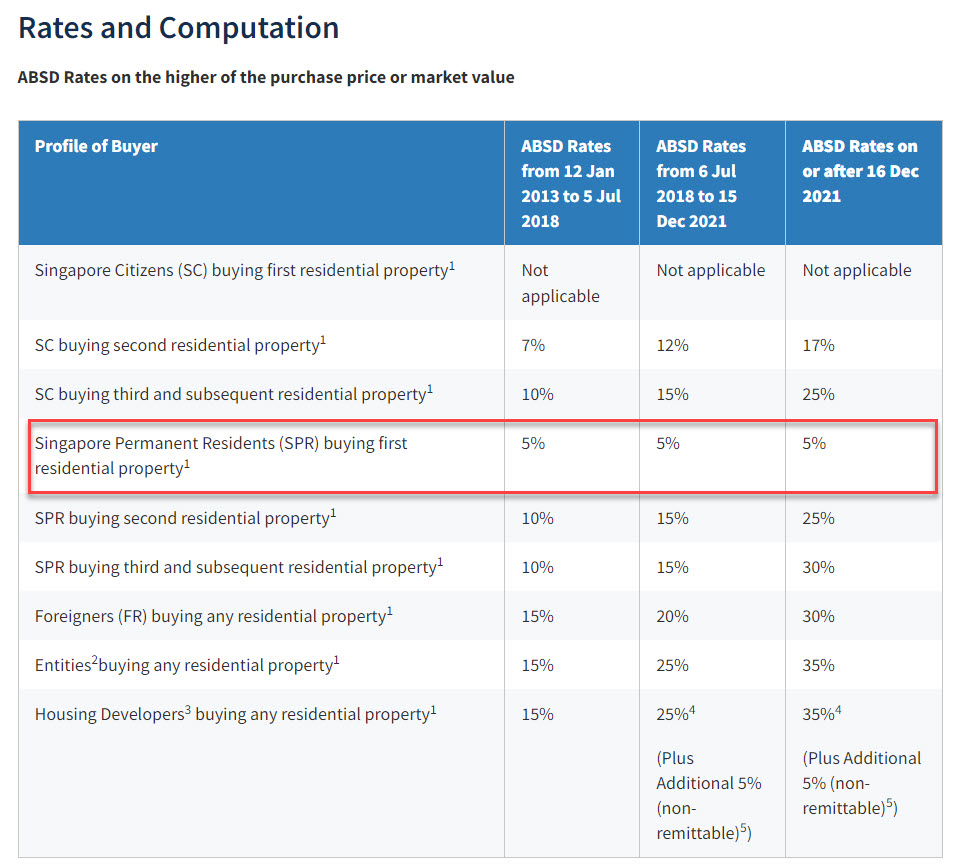

The tax regime in Singapore recognizes the difference between a Singapore PR versus a foreigner.

The gap is now much larger thanks to the introduction of property cooling measures on 16 December 2021.

For SPRs, the 5% ABSD rate for the first residential property remains.

For foreigners, the ABSD rate has been increased from 20% to 30% for their first residential property.

As a PR, this gap of 25% between you and a foreigner is a form of substantial tax benefit.

This presents an opportunity for you as you are essentially paying significantly lower taxes.

As someone who monitors the P&L statements of my clients’ property transactions, this means a significant addition to your bottomline.

A significant form of savings and gains.

Factor #4: Interest Rate Risks vs Rental Rate Risks

As a tenant, you are exposed to the risks of a landlord increasing the rental rates.

As a mortgage-paying property owner, you are exposed to the risks of the bank’s changing interest rates.

Both are risks and something for you to think about.

At this point, interest rates of 3% to 4% are considered high – especially after years of low interest rates.

This is something we can factor in our calculations if we take into account of the worst case scenarios.

We can calculate what happens if the banks decide to increase interest rate by another percentage.

But it is harder to calculate and predict – how much higher the rental rates a landlord can set.

Factor #5: Participate in the Growth of the Singapore Economy

Imagine, if you had bought a Singapore private property 10 years ago?

You probably would not be subjected to the whims of the landlord.

But more importantly, you have made significant gains and returns on your property.

Below is the Singapore Private Property Price Index. You can check it out here: https://data.gov.sg/dataset/private-residential-property-price-index-by-type-of-property

If you sincerely believe in the growth of the Singapore economy for the next 1-2 decades, this is a chance for you to participate.

The government of Singapore will continue to woo foreigners to come to Singapore.

Recently, they made some changes to the Global Investor Program to get companies to build and grow their presence here.

This new changes to the GIP means more good jobs and opportunities available for all who are willing to make Singapore their home.

Conclusion

Most Singaporeans already own a property. Like SPRs, they are taxed heavily if they try to go for a 2nd or 3rd property.

If you are SPR who have yet to own a Singapore property, this is a good time to consider.

If you have been working in Singapore for awhile, you would have accumulated your CPF monies that has yet to be deployed.

That can be a starting point to grow your retirement nest egg with returns larger than the CPF Board rate of 2.5%.

At the same time, you can avoid the relentless increase of rental prices.

If you are looking to explore your own property options in the Singapore market, I invite you to contact me for a no-obligation discussion.

Drop me a whatsapp message here: https://wa.me/6596588476/